Inflation has five primary causes

Milton Friedman was wrong

When I served in the state legislature, I was a goldbug. That is, I’d bought into the idea that central banks “printing money” caused inflation and the solution was to return to a gold-backed currency. I attempted to convince my committee to support legislation moving us in that direction, and when that failed, I took my arguments to the House floor with youthful exuberance. (The House was not persuaded.)

Like most theories which attempt to describe complex systems in a few words, the belief that printing money causes inflation is inaccurate. One simple proof of this is Bitcoin: new ones are created every 10 minutes, constantly inflating the supply. Despite this, Bitcoin suffers from deflation: the purchasing power of a coin has continued to grow. (Designed with a set-it-and-forget-it growth rate, Bitcoin can never hold a stable value, an essential feature of functional currencies.)

Yes, printing money can lead to inflation, as my younger goldbug self was fond of pointing out. Zimbabwe! Wiemar Germany! But in 2019 I had to recheck my basic assumptions after learning that the European Central Bank had failed for ten years to get inflation up to its 2% inflation target. Why would a central bank be unable to produce inflation?

It turns out inflation has many contributing factors. Before looking at the five primary ones, let’s try to define our terms.

What is inflation?

To describe a complex system inaccurately in a few words, inflation is prices going up. But which prices? As we’ve all seen, some products get cheaper over time (think TVs) while others get expensive (think cars). Other products fade away (think landlines) and new services appear (think Disney+). Which prices determine inflation?

Each month, the Bureau of Labor Statistics collects price data on 80,000 products in an evolving basket of goods and reports on how they’ve changed. This calculation comes in various flavors, because—and this is important—inflation is subjective, not objective. For example, inflation in February 2025 was lower than expected because of “a sharp decrease in airfares.” For the minority of Americans who fly each year, this is good, but for the majority, their expenses probably increased more than average. Official inflation numbers are imperfect, but they are still useful indicators.

Now, let’s look at the five primary causes of inflation as well as their deflationary counterparts:

1) Supply shrinkage

Egg prices are up 58% over last year. Is this because too many dollars have been manufactured? No, when bird flu wipes out millions of chickens, egg production shrinks. According to basic economics, prices are a reflection of the balance between supply and demand. (This is also an imperfect description of a complex system in a few words—there’s lots to learn after Econ 101.) When the demand for a product is greater than its supply, prices generally rise to reduce demand. At $8/dozen, some people will find substitutes, but for those who still buy eggs, their grocery bill has been inflated.

The flip side of this is demand shrinkage, which is what happened with airfare. With a few plane crashes in the news, some people are choosing not to fly. If the demand for a product is less than the supply, prices should fall to stimulate demand, and sure enough, airlines are cutting prices and creating deflation. (This is why individuals shunning environmentally damaging products are ineffective at reforming the structural convenience of pollution; withholding their demand incentivizes lower prices for everyone else.)

2) Cost push

When the business costs of producing a good or service increase, those costs are generally pushed forward onto the consumer. For example, the United States is considering wide-ranging tariffs, which are paid on goods by the importer. If imposed, customers may see prices inflated accordingly. Rising wages can have the same effect—after the Civil War, the supply of “free” labor vanished, and prices rose when formerly enslaved people had to be paid for their work.

The reverse of this is cost pull. In a competitive market, companies look for ways to reduce costs in order to pull prices lower, trading potential profits for market share. This is deflationary; even when costs rise, businesses may absorb some of them. (The tariffs in Donald Trump’s first term had minimal impact on inflation.)

3) Profit pull

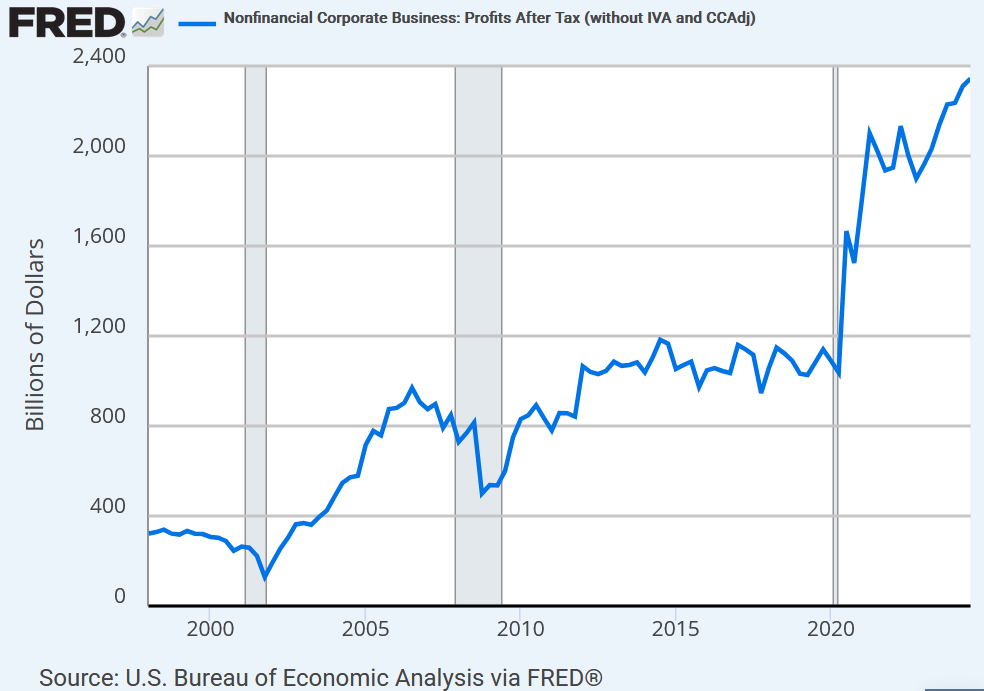

Sometimes businesses inflate their prices beyond any changes in their costs. This was widespread during the pandemic; in a single year, corporate profits doubled from $1,037 billion to $2,101 billion! That averages out to an additional $3,000 for every man, woman, and child in the United States; Matt Stoller calculated profit-pull inflation was responsible for 60% of total inflation in 2021.

This sort of behavior is more common during times of inflation, like 2021. When consumers are already expecting to pay more, companies have less incentive to compete on price. Rarely, deflation can spiral prices downward and create a different set of economic problems; in the Great Depression, the necessity to slash prices led to massive layoffs and 50% unemployment in some cities.

4) Artificial scarcity

A natural shrinking of supply can raise prices, like with eggs. But sometimes businesses purposely constrain production in order to create artificial scarcity and inflated prices. Diamonds are a classic example; there are an estimated 120,000 carets of diamonds for every person on the planet! De Beers, controlling 80% of the diamond supply, used artificial scarcity and marketing to persuade people these common gems had immense value.

In that case, a single company was able to corner the market, but the same technique can be used by multiple companies working in concert. This is illegal, but the laws against monopolistic behavior (antitrust) went unenforced or under-enforced for decades. (Donald Trump’s first term changed this with “relatively aggressive antitrust enforcement,” and Joe Biden continued it with his appointment of Lina Khan.) RealPage, for example, coordinates pricing among large landlords so they can leave apartments vacant and know the rest of the cartel will also restrict their supply, collectively reaping higher profits than if they’d lowered rent to fill the empty housing units.

Antitrust laws can’t be applied to foreign nations, which is how OPEC (Organization of the Petroleum Exporting Countries) is able to artificially restrict the supply of oil on the world market in order to drive the price—and their profits—higher. Last year, the Federal Trade Commission revealed evidence Texas oil fields were conspiring with OPEC to collectively restrain oil production and increase prices. Matt Stoller’s Substack (which I highly recommend) regularly highlights ways concentrated corporate power squeezes the economy. Addressing them with strong antitrust enforcement would be deflationary.

5) Demand pull

Last, let’s talk about demand-pull inflation. This is the classic fearmongering scenario around “printing money.” If the supply of goods and services in the market stays the same but people have more money to spend, demand may rise and drive up prices—inflation. (The Cantillon effect describes how the first to get new money reap an additional benefit, because they are able to spend it before prices rise.)

However, in a competitive market, it’s easy to see that these fears are overblown. If a grocery store has more people wanting to buy bread than loaves on its shelves, it will bake more, increasing supply to meet demand. If it refuses, trying to create artificial scarcity and higher prices, its would-be bread customers can go to a different store.

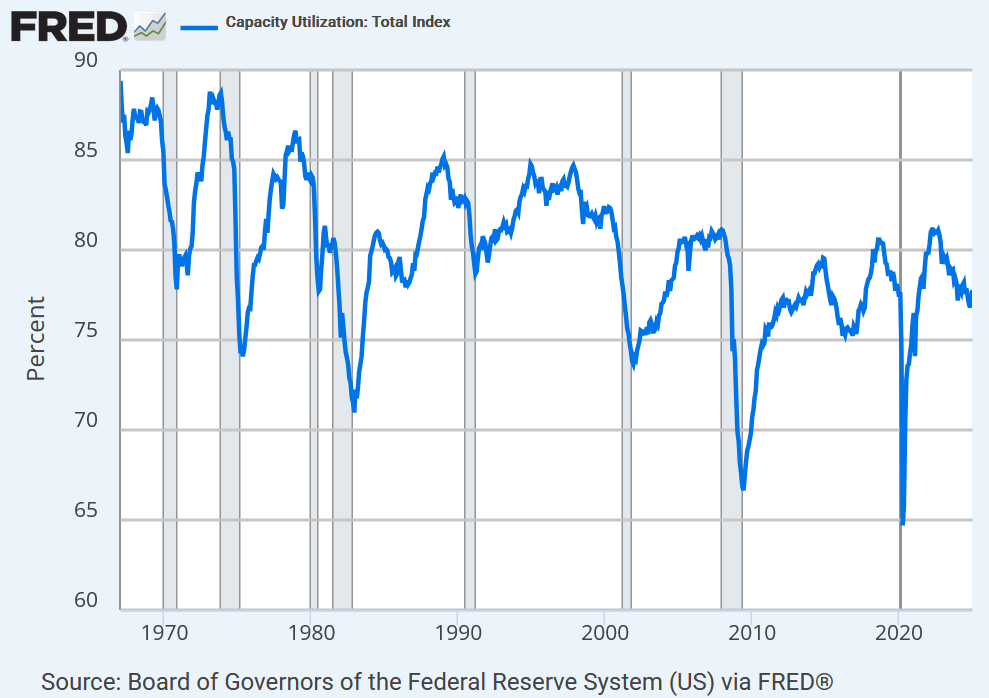

But what if all the ovens are being used to capacity, so it’s not possible to bake enough bread to meet demand? This is when demand-pull inflation rears its head; prices will rise until supply and demand are in balance. (It will also incentivize investment in new ovens, to better capitalize on the market imbalance.)

The Federal Reserve tracks the percentage of our productive capacity which is being utilized, and it’s easy to see it has trended downward for decades. The US has the ability to manufacture additional goods if demand increases; larger production runs spread fixed costs between more units, enabling prices to fall.

Conclusion

The economist Milton Friedman famously declared inflation is “always and everywhere a monetary phenomenon.” Even though he was wrong, many people still believe it. (Which I can understand, since I fell for it in my 20s.) Next time you hear “government spending is causing inflation,” remember there are many contributing factors—and that simple descriptions of complex systems are usually inaccurate!